Pharma Access with Chinese Characteristics

How policy shapes drug availability

This continues a series examining China’s role in the global biotech and pharmaceutical industry, and focuses on China’s drug markets. Our first piece explored the role of AI in China’s biotech ecosystem. Future articles will cover the Chinese biopharmaceutical research, innovation, and supply chains. If you have tips on any of these topics, please reach out.

As China prospers, so do its citizens’ expectations for high-quality healthcare. That means expensive drugs – but how can it make them affordable?

The government is transforming the landscape of China’s pharmaceutical markets, cutting drug costs, and pushing domestic firms to become more competitive. But even as policy advances, demand is evolving just as quickly.

As incomes rise, so does China’s disease burden. The country is seeing more of the chronic and complex illnesses common in wealthier nations — cancer, cardiovascular disease, and aging-related ailments — that often require expensive, innovative treatments. Forecast to grow to USD $264.5 billion in 2026, China’s pharmaceutical market is the second largest in the world behind the United States. The US is still by far the world’s largest pharma market, at over US$600 billion today.

China’s healthcare ecosystem remains challenged by corruption and other inefficiencies. Though domestic firms are improving, they are never going to fully meet the growing need for novel biotech and other expensive therapies. And though China’s new policy mechanisms have cut the price of many medications, they can’t keep patients, physicians, and companies happy all at once.

That means China continues to rely on imports for some of the most advanced treatments — those with high price tags that even aggressive government policy can’t cut away. For the sake of its citizens and broader social stability, China will have to navigate the difficult balance between affordability, access, and market power in the global pharmaceutical landscape.

The need for reform

In the 1990s, financial pressure to offset the losses from government funding cuts drove public hospitals to inflate prices and over-prescribe, causing widespread problems. The Chinese Food and Drug Administration (now known as the National Medical Products Administration, or NMPA) suffered from incompetence, corruption, and a large backlog of drug approvals. Pharmaceutical companies marked up drug prices and leveraged kickbacks1 to generate sales. In fact, generic drugs2 — which made up 95% of China’s drug approvals at the time — sold at gross profit margins of 80-90%.

At the same time, between 2009 and 2017, China’s total health expenditure on pharmaceuticals more than doubled, from 754.38 billion RMB to 1,820.3 billion RMB (or about $US110.45 billion to $268.76 billion).3

These trends were unsustainable for a growing China.

The Healthy China 2030 plan, unveiled in 2016, recognized the need for reform in the “three spheres” 三医 of healthcare, medical insurance, and pharmaceuticals.

To improve the quality of pharmaceuticals, the NMPA implemented Generic Quality Consistency Evaluations4 in 2015 to assess generic drugs relative to their original brand-name counterparts. In 2017, China joined the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH) and started adhering to the ICH-GCP (Good Clinical Practice) guidelines. Additional reforms streamlined and strengthened the drug approval regulatory process.

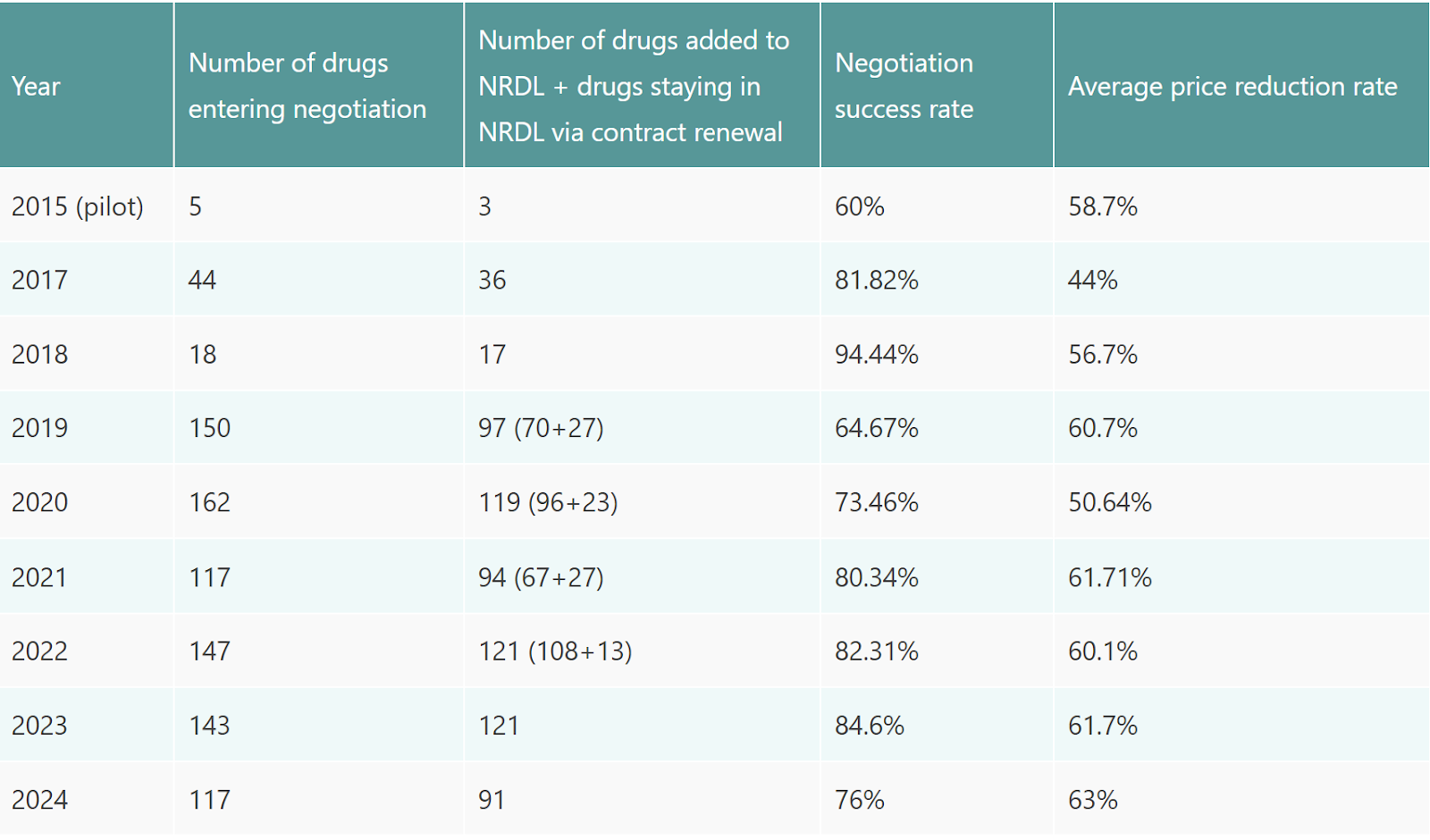

To improve the affordability of pharmaceuticals, China has begun to leverage two systems: the National Reimbursement Drug List (NRDL) and centralized volume-based drug procurement (CVBP).

National Reimbursement Drug List (NRDL)

Established in 2018, the National Healthcare Security Association 国家医保局 (NHSA) determines which patented drugs are included on the National Reimbursement Drug List (NRDL) and therefore covered under public health insurance schemes, which cover over 95% of China’s population to some degree.

How the NRDL works:

The NHSA assesses novel drugs based on safety, efficacy, affordability, and clinical value.

Drugs that demonstrate both high clinical value and low cost are categorized as Class A on the List and fully reimbursed by public insurance. Class B Drugs are clinically effective but higher cost, and thus only partially reimbursed.

Innovative drugs, orphan drugs, and drugs for rare diseases receive priority.

Nevertheless, innovative drugs that exceed a certain price threshold – including the most groundbreaking new cancer treatments – remain excluded.

The current 2024 NRDL includes 3,159 drugs, including 91 new additions.

Centralized Volume-Based Drug Procurement (CVBP)

The National Reimbursement Drug List improves access to clinically important drugs, especially new innovations.

China takes a more aggressive cost-cutting approach to generic medications. Piloted in 2018 and rolled out nationwide in 2019,5 the national centralized volume-based drug procurement system 国家组织药品集中采 combines the buying power of all public hospitals and leverages it to negotiate the lowest possible prices from suppliers.6

How CVBP works:

Every few months, the government7 invites suppliers to engage in a competitive bidding process for a selection of drugs.

Drugs submitted for bidding must first pass Generic Quality Consistency Evaluations, and then win by offering the lowest price.

Winning suppliers gain the right to sell a certain volume of medications — usually up to 70% of the previous year’s total consumption — to public hospitals. Domestic firms overwhelmingly win procurement rounds due to their ownership of raw-material manufacturing, large production capacities, and overall economics of scale.

The National Health Commission monitors hospitals and physicians to ensure that they prescribe bid-winning drugs.

Since the two pilot programs, the government has held 10 centralized volume-based procurement rounds and 8 iterations of the National Drug Reimbursement List and continues to fine tune both programs.8

Pills without the price pain

So, have the government’s programs worked?

If price reductions were the goal, then yes.

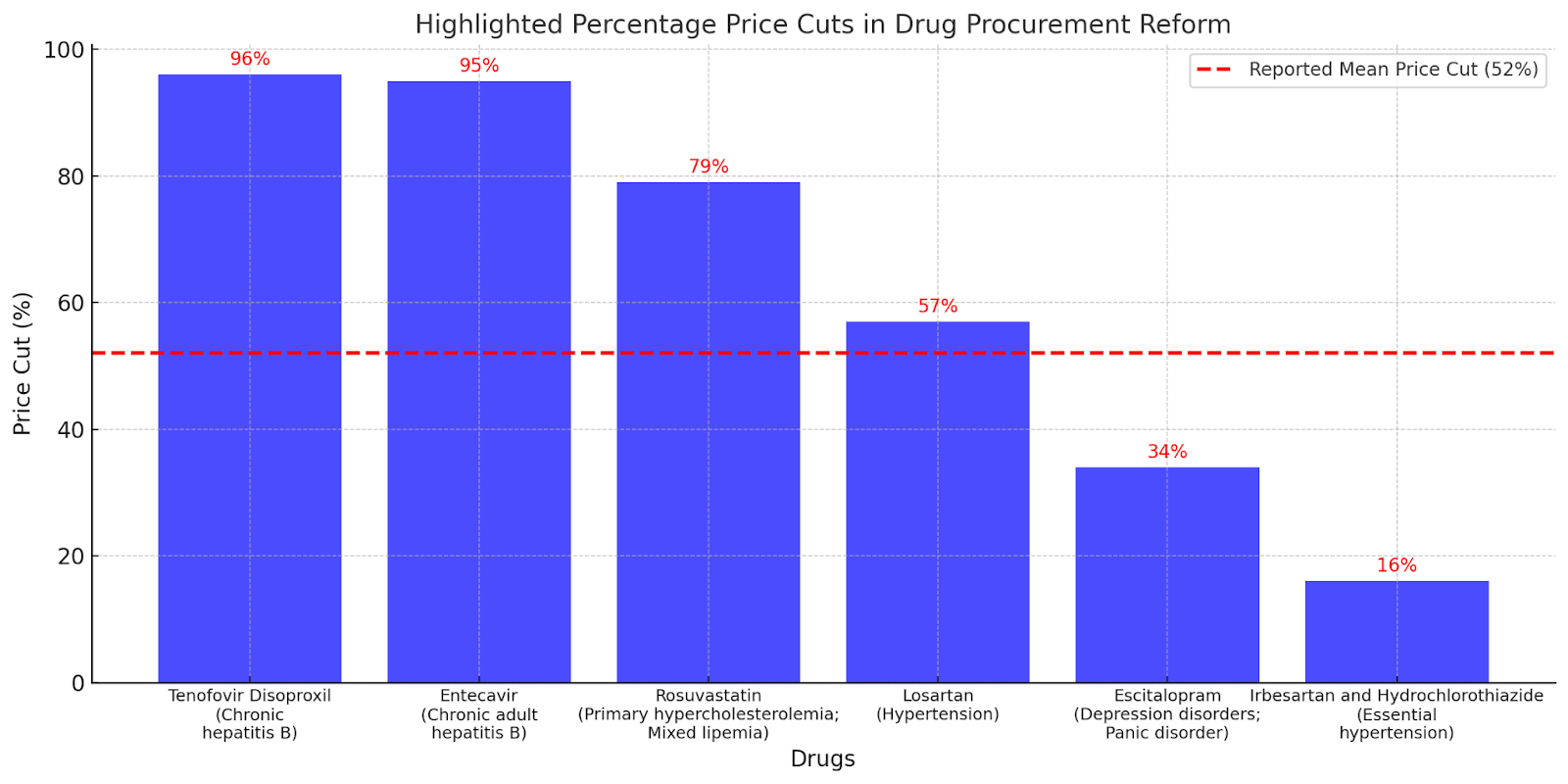

The National Drug Reimbursement List’s first round achieved price reductions of over 50% on treatments for chronic hepatitis B and lung cancer. Subsequent rounds achieved similar reductions in the 50-60% range, as the following chart indicates.

The pilot round of centralized volume-based procurement had similar results, with an average price cut of 52% for 25 drugs. A hepatitis B drug experienced the highest price cut — a whopping 96%, for a final bidding price of US$0.09 per tablet. That same drug would cost US$10.94 in the United States and US$15.84 in the United Kingdom.

The CVBP program has allowed China to access some of the lowest prices for generic drugs in the world.

Between 2018 and 2023, generic drug manufacturers cut prices to win contracts, on average, by over 50%, and sometimes over 90%. Studies of the “4+7” pilot show evidence that after a procurement round, consumption of quality-assured bid-winning drugs increases and overall drug spending decreases. Here are some notable examples:

Insulin: median price reduction of around 42% for a 2021 round applied to 42 insulin products — improving affordability9 and saving an estimated total of US$2.85 billion in the first year of contracts with the winning suppliers.

Lung-cancer treatment: price reduction by 83%, from 108 RMB to 18 RMB, saving patients an estimated 8,100 RMB per treatment cycle.

Stents to treat coronary heart disease: price reduction by 90%, from over 10,000 RMB (US$1,500) to around 1,000 RMB (US$150). As a result, the number of stents supplied to patients grew, and more medical institutions — including 500 additional second-tier hospitals10 — carried out stent implantation surgeries.

What do lower prices mean?

Government statistics estimated that as of 2022, CVBP created national savings of over 260 billion RMB (approximately $36.3 billion USD). The National Healthcare Security Administration (NHSA), which oversees public health insurance, reallocates over half of its savings from generic drug procurement to cover innovative medicines through the National Drug Reimbursement List.

In terms of affordability, one analysis of the pilot program’s impact found that the proportion of affordable drugs increased from 33% to 67%, and the mean affordability improved from 8.2 days’ wages to 2.8 days’ wages. Urban residents benefited more, a reflection of larger urban-rural healthcare disparities. In theory, improved affordability means patients are more likely and better able to adhere to their prescribed treatments.

Still, impacts on patient health outcomes have yet to be comprehensively evaluated. And the depth of the latest cuts has caused concern among both patients and physicians.

Saving cents, losing sense

In December 2024, the largest procurement round thus far resulted in the steepest price cuts yet, with some products discounted by over 90%.11 Not everyone was happy about this.

“You get what you pay for” is a common sentiment for consumers. So when generic aspirin tablets drop to an astonishing 0.03 RMB (US$0.0041) per pill, people start wondering what was sacrificed in pursuit of lower costs. On Chinese social media, patients have vocalized concerns that the generic drugs are less effective or cause more side effects.

One particular phrase by Zheng Minhua 郑民华 — surgeon-director of Shanghai Ruijin Hospital and member of the Chinese People’s Political Consultative Conference — went viral recently: “blood pressure doesn’t drop, anesthetics don’t bring sleep, and laxatives don’t release shit” 血压不降、麻药不睡、泻药不泻.

The phrase is part of a proposal submitted early this year by Zheng and his colleagues outlining concerns about the efficacy, reliability, and flexibility of bulk-procured generic drugs. Another doctor’s article — which has since been taken down — questions the validity of data published from evaluation trials of procured drugs.12 Some industry participants report that companies are able to replace excipients (non-active ingredients) of drugs after passing consistency evaluations without re-doing testing.

The government has since responded. However, these controversies come at a moment of broader frustration with China’s healthcare system, which stringent COVID-19 lockdown policies and sluggish post-pandemic economic recovery has only made worse.

Can you ever cure corruption?

Even with the government’s attempts to keep drug prices down, per capita medical costs have more than doubled in the last decade. While rising costs likely stem from a variety of systemic and economic factors, in China, corruption is a standout issue that the government can’t ignore.

In 2023, the National Health Commission initiated a crackdown on corruption, including bribery, misuse of insurance funds, rent-seeking by administrative officials, and unethical conduct. Over 160 hospital chiefs were detained.

Widely publicized, this anti-corruption campaign – which rewarded reports of corruption and the imposed strict monitoring of doctors – fueled distrust between the public and physicians.

Importantly, a majority of such medical corruption involves commercial bribery, in which pharmaceutical and medical suppliers give kickbacks to healthcare providers, leading to overprescriptions and inflated costs for patients. Legally, drug companies wield similar influence through heavy marketing, with one report showing that Chinese pharma companies had aggregate sales expenses of about 2.6 times that of R&D. Heavy workloads and low pay make doctors more receptive to drug suppliers’ incentives.

That pharmaceutical firms still turn to bribery and marketing to sway doctors suggests that government efforts to shape drug availability based on quality and cost have yet to fully succeed.

Despite the government’s efforts, domestic policy and industry still today falls short of the Chinese public’s desire for innovative drugs.

Imported drugs still matter

Accessing imported brand-name drugs can be a challenge — even if patients are willing to pay out-of-pocket. One reason may be Beijing’s focus on boosting Chinese drug manufacturers, actively cultivating their capabilities and favoring them during CVBP and NRDL selection processes.

This tension played out strikingly through Pfizer’s Paxlovoid, a treatment for severe COVID-19. Paxlovoid received conditional regulatory approval in February 2022 – so it was authorized to sell in China – but despite high demand, the drug never got included on the National Reimbursement Drug List.

So what happened during NRDL negotiations?

Officials cited Pfizer’s high asking price as the reason for no deal. Meanwhile, two COVID-19 treatments did make the list – the traditional Chinese medicine Qingfei Paidu and the domestically-produced antiviral pill Azvudine – reinforcing evidence of China’s preference for cheaper homegrown treatments.

Pfizer defended its price and rejected the notion of a future deal for domestic manufacturers to distribute a generic version of Paxlovoid in China, a common practice for low- and middle- income countries. “They are the second highest economy in the world and I don't think that they should pay less than El Salvador,” said CEO Albert Bourla at the time.

The Chinese public was left to deal with the fallout. Facing extreme shortages, people turned to the black market and to unproven Indian generic versions that sold for as much as 50,000 RMB, over twenty times the original price.

The case of Paxlovoid highlights both the extent of China’s progress and the gaps that still exist.

Yes, the domestic pharmaceutical industry is becoming increasingly formidable. But some important innovative drugs still remain beyond China’s borders, leaving it dependent on imports.

The Chinese government has made substantial – and in some cases, excessive – strides in ensuring medicine is affordable for its citizens. But novel pharmaceuticals come with high price tags that can’t be easily negotiated.

In 2024, the size of China’s innovative drug market13 reached a milestone of over 100 billion RMB (about USD $13.89 billion). Out-of-pocket payments or commercial health insurance covered over half of that market. It’s clear that China’s national medical insurance programs aren’t alone enough to meet China’s medical needs – especially if the goal is to provide the same level of care to its whole population that is expected in a G7 country.

Industry projections expect China’s combined market for innovative drugs and medical devices to exceed 1 trillion RMB (USD $137 billion) by 2035 – a full 30% of the global pharmaceutical market.

Is this a market opportunity for multinational companies? Or, will China be able to achieve its ideal world: a thriving domestic pharmaceutical ecosystem, managed by rigorous national insurance and bulk procurement programs, so that its citizens get the medicine they need.

Between the 1990s and 2018, provincial governments organized drug procurement. A “two-envelope” process awarded supplier status to pharma companies who met basic quality standards and offered the lowest prices. However, medical institutions retained the power to sign supplier contracts, which governments struggled to regulate. As a result, kickbacks, uneven access, and high drug costs continued.

A generic drug has the same active ingredient(s) and is bioequivalent to a brand-name drug, but is often more cost-effective and sold under a different name once the original drug’s patent expires.

As measured by China National Health Accounts. In 2017, drug spending made up 34.42% of China’s total health expenditure, meaning over a third of all healthcare costs were for medications.

The GCE tests generic drugs along two dimensions relative to their original brand-name counterparts, known as originators or innovators. The first is in vitro pharmaceutical equivalence (does it have the same active ingredient, dosage form, strength, and quality standards?) and in vivo bioequivalence (does it perform the same way in the body?). The US FDA and other regulatory bodies use similar frameworks to approve generic drugs. In 2017, the NMPA began adhering to international standards for pharmaceutical development and registration, which continues to this day.

The government’s “4+7” pilot was implemented in four municipalities and seven cities before rolling out nationwide in 2019. The 4 municipalities were Beijing, Shanghai, Tianjin, and Chongqing. The 7 cities were Guangzhou, Shenzhen, Xi’an, Dalian, Chengdu, and Xiamen. In total, they make up around one-third of the national market.

China’s use of pooled procurement for medicine pricing, by the way, is not unusual. Many countries, including Indonesia, Canada, and much of Europe, leverage bulk purchasing power and negotiations to reduce drug prices for public medical institutions.

The NHSA designs and oversees policy, the National Health Commission 国家卫健委 oversees hospitals, and the Joint Procurement Office (JPO) oversees implementation of centralized volume-based procurement, which is operated day-to-day by the Shanghai Pharmaceutical Centralized Bidding and Purchasing Management Office.

To mitigate risks of shortages, centralized procurement selection allows for multiple winners and runner-ups. In cases of medical necessity, hospitals may purchase a small number of drugs outside the program. And to compensate for lost income, hospitals receive government subsidies and charge higher service fees.

A study of the round assessed affordability as the number of daily wages needed by the lowest-paid unskilled government worker to obtain a 30-day supply, and found that insulin had changed from about 1.63 days’ wage to 0.68 days’ wage. Relative to costs of insulin in other countries, the reduction accomplished by China shows some improvement.

China’s hospitals are organized by a three-tier system based on their care, education, and research capacities.

778 products (the highest number of products so far) and 493 companies were involved in this procurement round.

The proposal points to evidence such as the fact that patients using bulk-procured anti-blood clot medication had higher incidence of strokes and pulmonary embolisms. It also expresses the need for greater flexibility given to physicians and hospitals if a bid-winning drug doesn’t apply to a specific medical case, or isn’t the right formulation (such as for pediatric use).

“Innovative drug market” includes newly developed pharmaceuticals that introduce novel mechanisms of action, significantly improve clinical outcomes, or address unmet medical needs. This market is typically measured by the revenue generated from patented, first-in-class, or breakthrough drugs.

This is a very clear exposition of the status of Pharma in China. One point to add is that there has been a flood of global biopharmaceutical companies in-licensing drugs from Chinese biotechs of late. This is noteworthy as we're talking new drugs (as opposed to cheap generics) and effectively China Inc is creating a pool of new assets that are competing (and in many ways displacing) those developed by Western Biotechs. They are also available at a clear discount. This phenomenon mirrors developments in other high tech arenas (such as AI).